Climate change risk reporting has so far been dominated by companies in carbon-intensive sectors like energy, mining and manufacturing and the institutions that finance and facilitate emissions from those sectors. For good reason, attention has focused on the scale and pace of decarbonisation needed to achieve the Paris Climate Agreement temperature goals and the “transition risk” this poses for the major companies, banks and investment firms whose decisions will largely determine whether those goals are met.

Comparatively, there is a “disclosure gap” when it comes to physical climate risk. A just-released review by the UNEP-FI of physical risk disclosure by financial institutions found that “the identification, measurement, and disclosure of climate-related physical risks by financial institutions are currently incomplete and inadequate for stakeholders to assess the extent of physical

risks facing these institutions and their clients.” The Institutional Investor Group on Climate Change two years ago observed that, “Investors who focus their strategic ‘climate change’ responses only on transition will be failing in their fiduciary responsibilities and may be creating legal liabilities.” A large number of companies have not yet come to terms with the material implications of unmitigated or poorly-mitigated climate change on their operations, their value chains and their financial position. Many that are investigating physical risk may not be fully disclosing what they know. A survey last year by the Taskforce for Climate-related Financial Disclosures found that only 42% of companies preparing disclosures were estimating a physical risk metric. Of these, only half were actually disclosing against that metric.

In its thematic review of climate and environmental risk, the European Central Bank observed that in general, “institutions place more emphasis on transition risks than on physical risks.” And yet, under the climate scenarios developed by the Network for Greening the Financial System, physical risks outweigh transition risks in all scenarios and all timescales. Central banks around the world are starting to speak publicly about the effects of climate change on fiscal outlooks, inflation, trade and investment.

What business has not been affected in some way by the floods, fires, droughts and heat waves across Europe, North America and the Asia-Pacific in the last two years, even only via inflationary pressures on food and the rising cost of insurance? Physical climate risk is already material and will intensify. Unlike transition risk, physical climate risk affects every company and it will not be short-lived.

Corporate leaders, lenders and investors are going to have to address the physical risk “disclosure gap” to avoid being caught unawares by asset impairment, escalating insurance premiums, lost productivity and disrupted supply chains. If physical risk is priced into financial markets before these disruptions worsen, it will have the added benefit of balancing the ledger with transition risk: companies who calculate the costs of decarbonisation, more finely than the costs of climate change, might perversely conclude the former is the greater risk.

Image credit: Climate Policy Institute 2022. Global Landscape of Climate Finance: A Decade of Data.

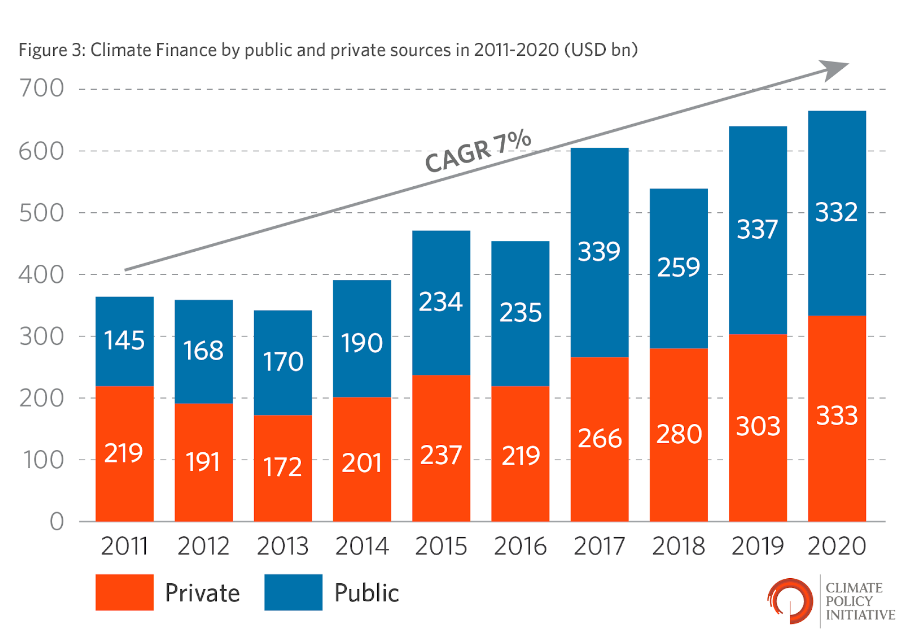

The gap in physical risk disclosure leaves people and whole societies vulnerable and capital investment that is unresponsive to physical risk could be capital burned, flooded or flattened by climate change. The flow of finance into responding to climate change is accelerating but compared to mitigation, the scale and quality of adaptation finance fall far short of needs. Every dollar spent on infrastructure, housing, energy and enterprise in the twenty-first century must be spent with climate resilience foremost in mind, to avoid large-scale capital destruction in the extreme floods, storms, heat and fire of climate change. Pricing physical risk will be crucial to this. In the coming year, physical risk analysis will need to become more comprehensive and be translated into metrics that accurately reflect the breadth, intensity and complexity of damage, disruption and loss climate change is likely to cause. XDI is ready and determined to bring consistent physical risk data to decision-makers at all scales for this reason.

It’s widely understood that climate change poses deep and lasting systemic risk, but most climate change risk disclosures are yet to fully reflect this, partly due to gaps in data and methodologies to turn complex, cascading and unbounded physical risks into financial metrics at the firm level. There is much more to compute, but it’s essential that we close the disclosure gap and bring the cost of climate change into the balance sheets of companies, banks, investors and governments before the bill is presented.